Paul’s charge to us in Romans 13:8 to owe nothing but love is a powerful reminder of God’s distaste for all forms of debt that are not being paid in a timely manner (see also Psalm 37:21). At the same time, the Bible does not explicitly command against all forms of debt. The Bible warns against debt, and extols the virtue of not going into debt, but does not forbid debt. The Bible has harsh words of condemnation for lenders who abuse those who are bound to them in debt, but it does not condemn the debtor.

Some people question the charging of any interest on loans, but several times in the Bible we see that a fair interest rate is expected to be received on borrowed money (Proverbs 28:8; Matthew 25:27). In ancient Israel the Law did prohibit charging interest on one category of loans—those made to the poor (Leviticus 25:35-38). This law had many social, financial, and spiritual implications, but two are especially worth mentioning. First, the law genuinely helped the poor by not making their situation worse. It was bad enough to have fallen into poverty, and it could be humiliating to have to seek assistance. But if, in addition to repaying the loan, a poor person had to make crushing interest payments, the obligation would be more hurtful than helpful.

PART ONE: SIX MEGABANKS’ RAP SHEET

At least $29 trillion was lent, spent, pledged, committed, loaned, guaranteed, and otherwise used or made available to bailout the financial system during the 2008 financial crash.1 The American people were told that this unprecedented rescue was necessary because, if the gigantic financial institutions, mostly on Wall Street, failed and went bankrupt (like every other unsuccessful private business in America), then they would take down the entire financial system, which would take down the U.S. economy, wreaking havoc on Main Street families. This was, we were told, primarily for two reasons. First, the collapse of Wall Street’s giants would result in a severe credit contraction where banks would not be able to provide credit inter mediation, which means taking deposits from tens of millions of American savers and using that money to make millions of loans. Second, their collapse would freeze the payments system and deprive all other businesses of the financial resources needed to run their companies and pay their employees.

That’s why, we were told, those financial giants were “too-big-to-fail”2 and “had to be bailed out” by taxpayers and the government. This has actually been true since the 1930s for traditional commercial and retail banks, primarily because they provide essential financial services like checking and savings accounts as well as loans to individuals and businesses small, medium, and large. That is the fuel for the American economy, standard of living, and overall prosperity, which is why those banks are insured by the FDIC and backed by the taxpayers.3 In addition, those banks were guaranteed because the odds of their failure were minimized—and taxpayers were protected—by numerous banking regulators 4 who policed their activities to promote safe and sound banking practices, making bailouts less likely. However, the $29 trillion in bailouts from the Fed, FDIC, and other regulators (in addition to the $700 billion taxpayer dollars made available under the TARP program) were not only or even – 3 – primarily provided to those regulated banks that take deposits and make loans.

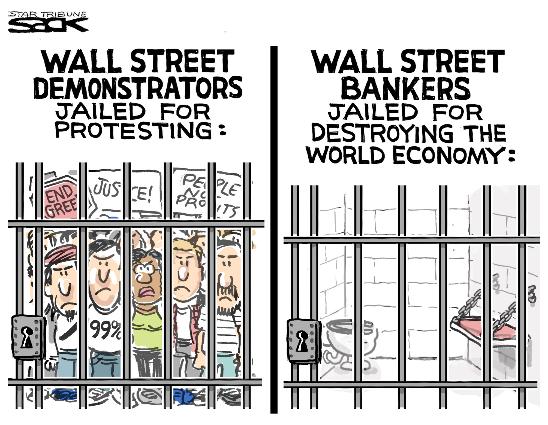

Instead, those bailouts were extended to virtually all financial institutions, including those engaging in the most dangerous, high-risk activities that actually caused the financial crash.5 Thus, for decades gigantic non-bank financial institutions like Goldman Sachs, Morgan Stanley, AIG, money market funds, and many more were allowed to maximize private profits with little or no regulation, but when their activities triggered the crash, they nonetheless were bailed out. This was a stunning violation of the most basic rule of capitalism, applicable to virtually every other business in America: Failure leads to bankruptcy. The largest bank and nonbank financial institutions were the beneficiaries of this double standard supposedly for one reason: to save hardworking Main Street Americans from the economic catastrophe that would have resulted from the collapse of the financial system and the economy. Indeed, policymakers claimed that, without bailing out the gigantic financial institutions, another Great Depression was almost inevitable, which would have been much worse than the Great Recession those financial institutions did cause—a recession that will cost the U.S. more than $20 trillion just in lost GDP.6 Of the more than $29 trillion in bailouts, just the six biggest banks in the country (the “Six Megabanks”) received more than $8.2 trillion in lifesaving support from American taxpayers during the 2008 financial crash, or nearly one-third of the total bailouts provided to the entire financial system.

This was a massive transfer of wealth from Main Street to Wall Street to prevent the bankruptcy of just six banks, supposedly because they were vital to the economic security and prosperity of Main Street Americans. One might think that receiving trillions of dollars of undeserved and lifesaving taxpayer bailouts would cause those financial institutions to reform their high-risk, destabilizing activities or, at a minimum, to rein in their predatory conduct and illegal practices. Think again. The banks showed no gratitude, no remorse, and no willingness to reform their activities.7 Worse, they also didn’t bother to end their systemic, widespread, and brazen illegal conduct. In fact, they have engaged in—and continue to engage in—a crime spree that spans the violation of almost every law and rule imaginable. Taking the breadth and depth of their illegal conduct as a whole, the six biggest banks in the country look like criminal enterprises with RAP sheets that would make most career criminals green with envy. That was the case not just before the 2008 crash, but also during and after the crash and their lifesaving bailouts, as detailed below.

In fact, the number of cases against the banks has actually increased relative to the pre-crash era. – 4 – – 5 – BANK OF AMERICA CITIGROUP GOLDMAN SACHS JPMORGAN CHASE MORGAN STANLEY WELLS FARGO 50 QTY 100 QTY $1 Billion $250 Billion $500 Billion $750 Billion $1 Trillion 80 71 34 71 41 54 $90,615,374,000 $20,003,462,000 $9,839,174,000 $38,862,236,000 $5,634,037,800 $16,954,118,00 $1,535,002,662,031 $2,920,896,888,595 $874,552,426,455 $460,982,382,326 $2,287,966,932,941 $198,712,559,776 Number of Major Legal Actions (QTY) Sanctions/Settlements Paid (Dollars) Government Bailout Money Received (Dollars) These Six Megabanks have committed hundreds of illegal acts and preyed upon and ripped off countless Main Street Americans with a frequency and severity that shocks the conscience. In fact, in the last two decades, while receiving more than $8.2 trillion in bailouts, these Six Megabanks have been subject to more than 350 major legal actions that have resulted in almost $200 billion in fines and settlements: 351 Major Legal Actions $181,908,491,800 Sanctions/Settlements $8,278,113

The violations giving rise to these major legal actions were serious and wide-ranging: Pre-crash: Bogus charges for credit monitoring services, overdrafts based on false balance information, illegal bid rigging, tricking subprime borrowers into buying credit insurance, selling unnecessary credit-card add-on products, providing conflict-ridden stock research analysis, trading ahead of clients, misrepresentations in the sale of auction rate securities, anticompetitive practices in the bond market, unlawful payment schemes to win muni-bond business, misallocation of public offering shares, antitrust violations, excessive overdraft fees on checking accounts, and opening millions of fake accounts; Crash-related: Fraud and abuse in the sale of mortgage-backed securities, loan servicing and foreclosure violations, betting against mortgage-backed securities that were sold to clients, use of invalid credit ratings for mortgage-backed securities, and steering subprime borrowers into more costly loans and falsifying income information; Post-crash: Unlawful debt collection practices, breach of fiduciary duty, market manipulation, anti-money laundering violations, unlawful securities lending practices, claims relating to the London Whale derivatives trades, abuses in the sale of credit monitoring services, error-ridden debt collection practices, failure to disclose adviser conflicts of interest, misrepresentations about foreign exchange trading programs, forcing clients into insurance policies, and kickback schemes involving title insurance.

U.S. taxpayers didn’t provide $8.2 trillion to bail out these banks and save them from bankruptcy in 2008 for them to continue the crime spree that actually caused the crash in the first place. These simply are not the types of banks—and these are not the types of activities—that should be backed by U.S. taxpayers. Moreover, it is clear that all these fines and settlements have been grossly inadequate. They have not been nearly enough to punish these banks for their prior illegal behavior or to deter them from engaging in future illegal conduct. In fact, it appears that these fines and settlements are just a cost of doing business, a speed bump on the road to ever larger bonuses, however they are generated.8

PART ONE: SIX MEGABANKS’ RAP SHEET Illegal Activity at the Nation’s Six Largest Megabanks Has Continued Since the 2008 Crash and Bailouts Six of the nation’s largest banks have amassed RAP sheets showing that the financial crash of 2008 did nothing to slow the pace of illegal activity that was well underway in the years leading up to the crash. All six of these megabanks were heavily engaged in illegal activity before the crash; they reached new heights of lawlessness in connection with the crash; and they continued to violate the law with abandon in the post-crash era. In fact, it’s gotten worse. Below are highlights of the major actions taken against the nation’s Six Megabanks since 2000, which addressed violations of law spanning roughly the last 20 years, from 1998 to 2018.

The cases have been grouped into three categories for each bank: Pre-Crash Actions, Crash-Related Actions, and Post-Crash Actions. Here is what the RAP sheet shows: 9 The NUMBER OF CASES against the banks HAS INCREASED relative to the pre-crash years, for all Six Megabanks. 9 The NATURE AND VARIETY OF THE VIOLATIONS throughout the period is ASTOUNDING, spanning virtually every conceivable type of white-collar crime, fraud, or breach of contract that a bank could commit. They encompass everything from fraud, money laundering, and market manipulation to foreclosure abuses, unlawful debt collection practices, antitrust violations, conflicts of interest, and kickback schemes. In short, these institutions have continued to commit frequent and serious violations of law, spanning an extraordinary variety of civil and criminal misconduct and resulting in tens of billions of dollars in penalties, civil judgments, and other monetary sanctions. The Six Megabanks have not skipped a beat when it comes to committing fraud, market manipulation, and other abuses against their clients, investors, and the financial markets themselves.

They continue to violate the law and to generate massive profits and huge compensation packages for their executives, without facing any meaningful punishment, deterrence, or accountability. – 8 – Six of the Nation’s Largest Banks The major legal actions against the nation’s six largest banks since 2000, which led to monetary sanctions in some form, have been catalogued. The banks include (1) Bank of America; (2) Citigroup; (3) Goldman Sachs; (4) JPMorgan Chase; (5) Morgan Stanley; and (6) Wells Fargo. The Three Groups The cases were grouped into three categories: • Pre-Crash, representing misconduct that occurred primarily before 2008 and was not related to the mortgage underwriting practices, residential mortgage-backed securities (“RMBS”) offerings, or foreclosure abuses directly tied to the financial crash; • Crash-Related, representing the core violations in the areas of mortgage underwriting practices, fraudulent RMBS offerings, and foreclosure abuses that helped trigger and fuel the financial crash; and • Post-Crash, representing misconduct that occurred primarily after 2008 and was not related to the financial crash.

Types of Actions. Included in the review were civil enforcement actions, administrative enforcement actions, and criminal actions at the federal level; state actions; and private litigation. These cases were brought by federal regulators and prosecutors; self-regulatory organizations (FINRA); state regulators; state attorneys general; private claimants; and others. Sanctions. The monetary sanctions reflected in the review include civil penalties, criminal penalties, disgorgement of ill-gotten gains, civil damages, re-purchase obligations, and other amounts such as consumer relief and mandated payments to public interest groups or causes. A conservative approach.

The list of actions taken against the Six Megabanks is undoubtedly conservative in that it does not include every governmental action taken against these banks in response to their illegal activities. In addition, it includes relatively few private lawsuits against the banks alleging financial fraud and other abuses. Hence, this survey actually understates the magnitude of the unlawful actions by the banks. The charts on the following pages set forth the collective RAP sheet for all Six Megabanks, along with more detailed summaries for each bank, including prime examples of the violations committed. Additional details about the actions and sanctions against the banks are available on Better Markets’ website, at www.bettermarkets.com. RAP Sheet Rundown1

The 6 Largest U.S. Banks – Collective RAP Sheet Total Actions: 351 – Total Sanctions: $181,908,491,800

Bank of America RAP Sheet Total Actions: 80 Total Sanctions: $90,615,374,000

Citigroup RAP Sheet Total Actions: 71 Total Sanctions: $20,003,462,000

Goldman Sachs RAP Sheet Total Actions: 34 Total Sanctions: $9,839,174,000

JPMorgan Chase RAP Sheet Total Actions: 71 Total Sanctions: $38,862,326,000

Morgan Stanley RAP Sheet Total Actions: 41 Total Sanctions: $5,634,037,800

Wells Fargo RAP Sheet Total Actions: 54 Total Sanctions: $16,954,118,000

Examples of the Six Megabanks’ Illegal Activities Massive Frauds that Fueled the Financial Crash With the tenth anniversary of the beginning of the financial crash, marked by the collapse of Lehman Brothers in September of 2008, now six months ago, it is worth remembering some of the most reckless and illegal activity conducted by these Six Megabanks that triggered and fueled the crash. Here is a just a brief overview, centered around rampant fraud in the offer and sale of countless residential mortgage-backed securities (RMBS). • Bank of America: In August 2014, the DOJ announced that it had reached a $16.65 billion settlement with Bank of America, resolving federal and state claims relating to financial fraud leading up to and during the financial crash. The bank “acknowledged that it sold billions of dollars of RMBS without disclosing to investors key facts about the quality of the securitized loans… The bank has also conceded that it originated risky mortgage loans and made misrepresentations about the quality of those loans to Fannie Mae, Freddie Mac and the Federal Housing Administration.” • Citigroup: In July 2014, Federal and State authorities secured a $7 billion settlement with Citigroup “for misleading investors about securities containing toxic mortgages.” Citigroup acknowledged that it seriously misrepresented the nature of the mortgage loans it securitized and sold in the years leading up to and during the financial crash, prompting the DOJ to announce that the “bank’s activities contributed mightily to the financial crisis that devastated our economy in 2008.” Earlier, in October 2011, the SEC charged Citigroup with misleading investors about a $1 billion Collateralized Debt Obligation (CDO) tied to the housing market. This CDO defaulted only a few months after being sold, and Citigroup paid a $285 million fine to settle the charges. • Goldman Sachs: In April of 2016, the DOJ, along with other federal and state regulators, announced a $5 billion settlement with Goldman Sachs for its part in packaging, securitizing, marketing, and selling RMBS in the years leading up to the crash. The settlement makes clear that the bank falsely assured investors that its RMBS were backed by sound mortgages, when it knew that they were in fact full of mortgages likely to fail. Earlier, in July 2010, Goldman Sachs agreed to pay $550 million to settle SEC charges that the firm misled investors in the sale of a mortgage-backed security called Abacus 2007- AC1. The SEC charged “that Goldman misled investors in a subprime mortgage product just as the US housing market was about to collapse.” In agreeing to pay the penalty, Goldman “acknowledged that its marketing materials for the subprime product contained incomplete information.”

• JPMorgan Chase: In November 2013, the DOJ, along with other federal agencies and six states, reached a settlement with JPMorgan Chase for $13 billion over its fraudulent sale of RMBS. As the DOJ observed when announcing the settlement, the bank was “packaging risky home loans into securities, then selling them without disclosing their low quality to investors,” eventually “sow[ing] the seeds of the mortgage meltdown. Earlier, in November 2012, JPMorgan Chase and Credit Suisse agreed to pay a combined $417 million to settle SEC charges that the two firms misled investors in the sale of nearly $2 billion in troubled mortgage securities. The director of the SEC’s Division of Enforcement observed that “misrepresentations [like these] in connection with the creation and sale of mortgage securities contributed greatly to the tremendous losses suffered by investors once the U.S. housing market collapsed.”

• Morgan Stanley: In February of 2016, Morgan Stanley agreed to pay a $2.6 billion penalty to settle DOJ allegations that the bank had sold billions of dollars in subprime RMBS to investors while making false claims about the underlying mortgage loans and knowing that many of the loans backing the securities were toxic. • Wells Fargo: In August of 2018, Wells Fargo agreed to a settlement with the DOJ requiring the bank to pay $2.09 billion for its role in the fraudulent origination and sale of subprime residential mortgage loans, which led to billions of dollars in losses among investors. The agreement revealed that Wells Fargo actually conducted repeated internal testing showing that over half of the loans in question had flaws for which there was no plausible explanation, yet the bank withheld that information from investors and the public

. • Multiple Banks: In March 2012, the five largest mortgage-servicing companies—JPMorgan Chase, Citigroup, Bank of America, Wells Fargo, and Ally Financial (the successor to GMAC)—entered a $25 billion settlement with the U.S. DOJ and 49 state attorneys general to resolve a host of abusive servicing and foreclosure practices. Principal among them was the mass-signing of affidavits to be filed in court that were required to foreclose on homes in states with a judicial foreclosure process; although the signers were swearing under oath that they had personal knowledge that the foreclosure was valid, they were in fact automatically signing the affidavits without reviewing any of the underlying documentation to ensure its accuracy. In short, they were lying under oath and committing a fraud on the court system. Unsurprisingly, these affidavits routinely got many of the facts wrong, leading to countless improper foreclosures.

This was the most massive perjury conspiracy in the history of the country. – 18 – The Beat Goes On: Major Violations of Law Continue to the Present Day Even after this series of historically large settlements and sanctions resulting from the Six Megabanks’ pervasive frauds, which were largely responsible for the worst financial crash since the Great Depression, the banks have apparently learned little. Since the crash, these banks have continued to engage in a wide range of illegal activities. Here are some of the most prominent examples. Reckless derivatives trading by the London Whale. In May 2012, JPMorgan Chase revealed that it had sustained an estimated $2 billion in losses associated with a series of complex credit default swap (CDS) transactions made through its London branch. It was later revealed that the losses exceeded $6 billion. JPMorgan Chase agreed in September 2013 to pay a combined $920 million in penalties to U.S. and U.K. authorities for engaging in “unsafe and unsound practices.” The following month, the bank agreed to pay $100 million in fines to the CFTC because, by pursuing an aggressive trading strategy, its “traders recklessly disregarded” the principle that markets should set prices.

This illegal conduct is particularly worrisome because it shows that only a few years after 2008, JPMorgan Chase was once again engaged in the type of large-scale, risky, proprietary trading in complex derivatives that contributed to the financial crash. While the direct losses exceeded $6 billion, the resulting loss to JPMorgan Chase’s stockholders in market value exceeded $22 billion. Manipulation of the LIBOR benchmark interest rate. Beginning in 2012, international authorities conducted a lengthy investigation into a widespread plot by multiple banks, including Citibank and JPMorgan Chase, to manipulate the London Interbank Offered Rate, or LIBOR, for profit. LIBOR underpins over $300 trillion worth of loans worldwide, including home, auto, and personal loans affecting virtually every American.

The scandal shook trust in the global financial system. Regulators in the United States, United Kingdom, and European Union have fined banks more than $9 billion in response. An assistant attorney general referred to the scandal as “epic in scale, involving people who have walked the halls of some of the most powerful banks in the world.” Citigroup is the latest megabank to pay a penalty for manipulating LIBOR and related indices, having admitted to reporting consistently false information during a period in 2010 in order to maximize profit. It paid a $175 million civil penalty to the CFTC for its part in manipulating LIBOR. Excessive insurance fees resulting from a kickback scheme.

In February 2014, Bank of America settled a class action lawsuit brought by homeowners who had a mortgage loan through Bank of America or Countrywide Home loans and ended up with force-placed insurance. Class members alleged that Bank of America and Countrywide violated state and federal laws, including the U.S. Racketeering Influenced and Corrupt Organizations Act, when the banks charged excessive insurance fees in order to cover the cost of kickbacks received from insurance providers. The lawsuit, filed in 2012, provides relief to customers that were charged for forceplaced insurance between January 2008 and February 2014. – 19 – Manipulation of the foreign currency market. In May of 2015, the DOJ announced that Citigroup, JPMorgan Chase, Barclays and Royal Bank of Scotland had agreed to plead guilty to charges of conspiring to manipulate the price of U.S. dollars and euros exchanged in the foreign currency exchange spot market.

Together, the banks agreed to pay criminal fines of more than $2.5 billion. Attorney General Loretta Lynch referred to their conduct as “egregious.” Another official castigated the banks for “undermining the integrity and competitiveness of foreign currency exchange markets.” These violations sound esoteric, but they impacted virtually every consumer in the United States because the FX markets are used by virtually every company producing goods that are purchased in the U.S. The FX markets are also used by and in connection with anyone traveling overseas. All those people were likely victims of this scheme to rig the FX markets. Illegal credit card practices. In July of 2015, the CFPB issued a consent order imposing sanctions against Citibank for deceptive and unfair practices in connection with credit card add-on products and services, which lasted from 2000 to 2013. The CFPB explained that the bank had engaged in a pattern of misrepresenting the costs, fees, and benefits of the products and had illegally enrolled customers for the services. The order imposed $700 million in monetary relief for the benefit of 8.8 million affected customer accounts. Fraud and breach of fiduciary duty.

In December of 2015, the SEC announced the imposition of $267 million in penalties against JPMorgan Chase for fraud, failure to disclose conflicts of interest, and breach of fiduciary duty by its wealth management units. Those units failed to disclose that they operated various investment programs with a preference for proprietary funds and third-party managed private hedge funds that shared client fees with a JPMorgan Chase affiliate. The misconduct extended from 2008 to 2013. Manipulation of the “U.S. Dollar ISDA Fix.” In December of 2016, the CFTC issued a consent order against Goldman Sachs for its attempts to manipulate a leading global benchmark used to price a range of interest rate derivatives, all for the benefit of Goldman’s trading positions. The violations extended from 2007 into 2012, and involved multiple traders, including the head of the bank’s interest rate products trading group in the U.S. The sanctions included a $120 million civil penalty. Overdraft fees. In September of 2018, a federal judge approved a class action settlement to resolve claims that Bank of America improperly charged overdraft fees amounting to interest, which when annualized far exceeded the limits on maximum interest rates set by the National Bank Act. The settlement required the bank to pay over $66 million in reimbursements and debt relief.

Unsuitable investment recommendations. In February of 2017, the SEC announced a settlement with Morgan Stanley for recommending complex inverse ETF investments to clients with retirement and other accounts without ensuring that those investments were suitable. In some instances, the bank failed to obtain documents signed by clients acknowledging the special risks and features surrounding those products. Under the agreement, the bank agreed to pay an $8 million penalty. Customer abuses, kickbacks, and discrimination.

Wells Fargo has engaged in a truly breathtaking series of violations that are unrelated to the financial crash, some of which began years before the crash while others are of more recent vintage. It includes, first and foremost, an illegal pattern and practice of ripping off millions of customers by fraudulently opening and funding bogus accounts with stolen customer money. It began more than 15 years ago and since then, thousands of Wells Fargo employees in hundreds of branches around the country appear to have engaged in illegal, if not criminal, business practices involving fraud, identity theft, falsification of the banks’ books and records, fabrication of customer account information, and the unauthorized charging of fees and debiting of accounts, all in connection with opening millions of bank and credit card accounts their customers did not know about.

Wells Fargo settled the coordinated action of the CFPB, the OCC, and the Los Angeles City Attorney in September 2016 for $185 million in monetary sanctions. In May of 2018, a federal judge approved a $142 million settlement for the benefit of customers who paid improper fees or were otherwise harmed by the fake-accounts scandal. And in September of 2018, another federal judge approved a $480 million settlement in a class action brought by Wells Fargo shareholders who suffered losses after the fake-account scandal came to light. That was only the beginning. Immediately after the crash of 2008, Wells Fargo continued to cheat customers. In 2015, Wells Fargo settled allegations that, between 2009 and 2013, the bank was involved in an illegal marketing-services-kickback scheme with Genuine Title, LLC, which provided Wells Fargo’s loan officers with cash, as well as consumer information and marketing services aimed at helping them drum up more loan business.

In return, the loan officers referred real estate settlement service business to Genuine Title. The proposed consent orders require $24 million in civil penalties from Wells Fargo and $10.4 million in redress to consumers whose loans were involved in this scheme. In July 2012, the bank settled DOJ allegations that it engaged in a pattern or practice of discrimination against qualified African-American and Hispanic borrowers in its mortgage lending from 2004 through 2009. The final price tag was $203 million. In 2018, Wells Fargo was ordered to pay $1 billion to the CFPB and OCC to settle allegations that Wells Fargo violated the Consumer Financial Protection Act in its administration of a mandatory insurance program related to its auto loans and in how it charged certain borrowers for mortgage interest rate-lock extensions. Wells Fargo was ordered to re-mediate harmed consumers and undertake certain activities related to its risk management.

PART TWO: THE SIX MEGABANKS’ BAILOUTS

Overview The $8.2 trillion in bailouts for these Six Megabanks were made through a bewildering array of emergency rescue programs hastily created by Congress or the banking regulators in connection with the 2008 financial crash and economic crisis it caused. These programs were essential for the very survival of these Six Megabanks, each one of which would have failed and gone bankrupt but for the bailouts.64 These bailouts, policymakers claimed, were only done out of conviction that their failure would lead to a collapse of the entire financial system and economy. In the sections that follow, we set forth the various bailout programs that saved the banks from themselves and the amounts of funding, lending, or other forms of assistance that each of the Six Megabanks received.

However, before the specific numbers are discussed, it is important to dispel one of the pernicious myths surrounding the bailouts: the claim that, because emergency funds actually expended or disbursed were returned to Treasury and the Fed and/or that fees were collected from the banks and nonbanks under some of the programs, the bailouts actually turned a profit for the American taxpayer or were, as so many claim, “profitable.” As detailed in Better Markets’ report on the $20 trillion cost of the crisis,65 this claim rests on the ludicrous assumption that a one penny “return” on even trillions of dollars somehow equates to a profit.

That ignores the fundamental standard to which all financial institutions, including Wall Street’s Six Megabanks, adhere: A return can only be evaluated if it is risk-adjusted and, in this case, the government should have but never did receive any risk-adjusted returns on any of the funds expended, disbursed, guaranteed, or otherwise used in any form or manner. Compare that to the risk-free rate of return of more than 60% received by Warren Buffett on his “investments” in Goldman Sachs. This myth is not only false but also dangerous because it belittles and understates the damage the crash caused to the economy and Americans’ quality of life and promotes a sense of complacency that increases the likelihood of another crash. The Bailout Programs That Rescued the Banks Before, during, and after the bankruptcy of Lehman Brothers on September 15, 2008, there was a sudden proliferation of unprecedented emergency legislative and regulatory programs designed to rescue failing banks, restore liquidity to frozen credit markets, and reassure the American public that the economy would survive.

Those programs fell into two broad categories: the relatively small $700 billion TARP program and the tens of trillions of dollars in Non-TARP programs. Within each of those groupings, a wide variety of rescue programs were established, many of which benefited the Six Megabanks. The bailouts took multiple forms, including asset purchases, repeated access to lending facilities on extraordinarily favorable terms, overnight conversion of investment banks into bank holding companies, and guarantees or backstops. Although many more funding facilities were created to bailout the financial system, the eleven key programs that the Six Megabanks relied upon most to survive are described on the following pages. TARP Just weeks after Lehman Brothers crashed, on October 3, 2008, Congress enacted the “Emergency Economic Stabilization Act of 2008,” which created the “Troubled Asset Relief Program,” or TARP. It authorized the Treasury Department to spend as much as $700 billion of taxpayer money to bail out the banks through capital injections or related programs. It had several components: • Capital Purchase Program (CPP): First activated on October 28, 2008, this was viewed as the primary initiative under TARP for stabilizing banks, financial markets, and the financial system. It was designed to provide new capital to failing, near-failing, or stressed banks through the government’s purchase of senior preferred shares, thereby injecting new capital into the banks.

Over 700 financial institutions participated in the program,66 including each of the Six Megabanks. • Targeted Investment Program (TIP): Announced in late November of 2008, this was a TARP initiative that Treasury established as an additional measure to prevent the failure of Citigroup and, later, Bank of America.67 • Making Home Affordable (MHA): This was a Treasury program under TARP designed to help struggling homeowners prevent avoidable foreclosures by providing incentive payments to promote mortgage loan modifications and other foreclosure alternatives.68 This program, one of the few programs intended to provide relief directly to Main Street Americans rather than Wall Street banks, was underutilized and a massive failure. • Term Asset-Backed Securities Loan Facility (TALF): Authorized on November 24, 2008, this was a joint Treasury and Federal Reserve program involving TARP as well as the Federal Reserve’s emergency authority under Section 13(3). It was designed to bail out the assetbacked securitization markets. The program provided non-recourse loans to companies and individuals in return for collateral in the form of securities, including asset-backed securities, that could be forfeited in the event of default on the loans.

The goal was to bail out the frozen secularization markets. The argument was that this would lower interest rates for auto loans, student loans, small business loans, credit cards, and other consumer and business credit.69 – 22 – – 23 – NON-TARP Many non-TARP programs were established to help rescue failing banks. Most were set up and administered by the Federal Reserve (often purportedly pursuant to its emergency powers under Section 13(3) of the Federal Reserve Act), but other federal agencies, such as the FDIC, also extended or participated in non-TARP bailout programs as well. Section 13(3), rarely used before the crash, gave the Federal Reserve authority to extend credit to individuals, partnerships, and corporations “under unusual and exigent circumstances.” The non-TARP programs benefiting the Six Megabanks included: • Term Auction Facility (TAF): Announced on December 12, 2007, this was a Federal Reserve program under existing Federal Reserve Act authority designed to address disruptions in the interbank lending markets.

It revised requirements governing lending from the Federal Reserve’s discount window, and established an auction system through which eligible depository institutions could obtain funding using a wider range of collateral than normally permitted. One benefit was that the auction format allowed borrowing institutions to reduce the risk that creditors or counterparties would perceive resort to the discount window as a sign of distress.70 • Term Securities Lending Facility (TSLF): Announced on March 11, 2008, this was a Federal Reserve program under Section 13(3) (its first use during the crash) that auctioned 28-day loans of U.S.

Treasury securities to primary dealers, in exchange for less liquid securities such as RMBS. The intent was to promote confidence among lenders and to lessen the need for dealers to sell illiquid assets into the market, which would aggravate downward price spirals.71 • Primary Dealer Credit Facility (PDCF): Authorized on March 16, 2008, this was a Federal Reserve program under Section 13(3) that provided overnight cash loans, secured by a broad class of eligible collateral, to primary dealers facing strains in the repurchase agreement markets.72 A primary impetus for this program was to afford immediate relief in an effort to forestall a Bear Stearns bankruptcy that was anticipated on March 17, 2008. • Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility (AMLF): Announced on September 19, 2008, this was a Federal Reserve program under Section 13(3) that provided liquidity support to money market mutual funds facing redemption pressures.

The program authorized loans to discount window eligible depository institutions and their primary dealer affiliates to purchase asset-backed commercial paper from money market mutual funds (“MMFs”).73 This provided a source of cash with which MMFs could meet increasing redemption demands without having to sell asset-backed commercial paper into an illiquid and distressed market, thus avoiding further downward pressure on the value of those assets. (This program was complemented by another initiative, the Money Market Investor Funding Facility, which funded the purchase of a broader range of short-term debt instruments held by MMFs. In addition, in September of 2008, after the Reserve Primary Fund broke the buck, Treasury announced a complete guarantee of over $3 trillion in money market fund deposits, known as the Money Market Mutual Fund Guarantee Program.) – 24 – • Commercial Paper Funding Facility (CPFF): Authorized on October 7, 2008, this was a Federal Reserve program under Section 13(3) designed to restore liquidity to the commercial paper markets.

It established a special purpose vehicle, funded with government loans, that stood ready to purchase both asset-backed commercial paper and unsecured commercial paper, thus ensuring the issuers would be able to issue new paper to replace their maturing obligations.74 • Temporary Liquidity Guarantee Program (TLGP): Announced on October 14, 2008, this program was created by the FDIC under its standing authority. It had two components, the Debt Guaranty Program (DGP) and the Transaction Account Guarantee Program (TAG), both designed to support liquidity and prevent runs in the banking system.

The DGP guaranteed bank debt, and the TAG insured all non-interest-bearing deposit accounts in full, extending FDIC deposit insurance beyond the $250,000 deposit insurance limit for those accounts.75 The primary beneficiaries of TAG were accounts used by businesses and local governments, such as payroll processing accounts. • Agency Mortgage-Backed Securities (MBS) Purchase Program: Announced on November 25, 2008, this program involved the Federal Reserve’s large-scale purchase of agency MBS from primary dealers via open market operations for the purpose of supporting the housing market and the broader economy. It was established pursuant to non-emergency authority in the Federal Reserve Act. The Bailout Breakdowns A number of reports have been issued cataloguing the bank bailouts during the financial crash under the TARP and non-TARP programs.

This report relies primarily on two sources: (1) ProPublica’s “Bailout Tracker” describing the elements of TARP and the recipients of all monetary support made available under TARP76; and (2) the GAO’s extensive summary and analysis of the Federal Reserve’s numerous non-TARP programs that provided financial support for banks and other institutions, issued in July of 2011.77 In addition, we supplemented that data with information set forth in the FDIC’s analysis of the response to the crash78 and a public policy brief issued by the Levy Economics Institute of Bard College in 2012.79 The estimates set forth below are conservative in a number of respects.

First, comprehensive data showing the precise amount of bailout funding for each bank under each program is not readily available. For example, complete data on the level of participation by the Six Megabanks in the Agency Mortgage-Backed Securities Purchase Program has not been made readily available, apart from the amounts reported for Citigroup and Morgan Stanley. It is clear, however, that other banks participated as well. In addition, some guarantee programs provided benefits to the banks but never actually resulted in the transfer of funds.

For example, in late November of 2008, Treasury established the Asset Guarantee Program under TARP. It was designed to backstop the guarantee of $301 billion pool of Citigroup assets, but it was never drawn upon. (A similar arrangement was struck with Bank of America regarding a $118 billion pool of assets, but it was never finalized.) Citigroup undoubtedly benefited from having the guarantee in place as part of the – 25 – third restructuring of Citi’s lifesaving bailout package,80 but it is impossible to accurately monetize the value of that benefit or the corresponding cost to the government for purposes of totaling bank bailout funding. Similarly, the Federal Reserve’s authorization of the overnight conversion of the Goldman Sachs and Morgan Stanley investment banks into bank holding companies, thereby giving them immediate access to the full panoply of rescue programs, was unquantifiable but priceless.

There is no doubt that, but for this action, both banks would have gone bankrupt, as revealed by the following internal email at the New York Fed describing a discussion with Morgan Stanley (“MS) about it and Goldman Sachs (“GS”) on September 20:81 As detailed in the summary charts on the following pages, the Six Megabanks collectively received at least $8,278,113,852,124 in bailout support during the financial crash, under a multitude of programs. Citigroup topped the list, having received the staggering sum of over $2.6 trillion in bailout support. Wells Fargo, at the bottom of the list, still received the extraordinary amount of over $170 billion.

Total Bailout Funding for All Six Megabanks: $8,278,113,852,124 Non-TARP Primary Dealer $5,581,000,000,000 Credit Facility (PDCF) Term Securities $857,000,000,000 Lending Facility (TSLF) Term Auction $648,000,000,000 Facility (TAF) Temporary Liquidity $427,190,613,124 Guarantee Program (TLGP) Agency Mortgage- $390,660,000,000 Backed Securities Purchase Program (MBS) Asset-Backed $114,000,000,000 Commercial Paper Money Market Mutual Fund Liquidity Facility (AMLF) Commercial Paper $52,000,000,000 Funding Facility (CPFF) AIG Counterparty $30,100,000,000 TARP Capital Purchase $120,000,000,000 Program (CPP) Targeted $40,000,000,000 Investment Program (TIP) Making Home $9,163,329,000 Affordable (MHA) Term Asset- $9,000,000,000 Backed Securities Loan Facility (TALF) TOTAL TARP $178,163,239,000 TOTAL Non-TARP $8,099,950,613,124 Sources: ProPublica Bailout Tracker; GAO-11-696; Crisis and Response: An FDIC History, 2008-2013; Levy Economics Institute of Bard College – 27 –

Total Bailout Funding for Bank of America $1,535,002,662,031 Capital Purchase $25,000,000,000 Program (CPP) Targeted $20,000,000,000 Investment Program (TIP) Making Home $2,160,000,000 Affordable (MHA) Primary Dealer $947,000,000,000 Credit Facility (PDCF) Term Securities $101,000,000,000 Lending Facility (TSLF) Term Auction $280,000,000,000 Facility (TAF) Temporary Liquidity $130,842,662,031 Guarantee Program (TLGP) Asset-Backed $2,000,000,000 Commercial Paper Money Market Mutual Fund Liquidity Facility (AMLF) Commercial Paper $15,000,000,000 Funding Facility (CPFF) AIG Counterparty $12,000,000,000 TOTAL TARP $47,160,000,000 TOTAL Non-TARP $1,487,842,662,031 Non-TARP TARP – 28 –

Total Bailout Funding for Citigroup: $2,920,896,888,595 Capital Purchase $25,000,000,000 Program (CPP) Targeted $20,000,000,000 Investment Program (TIP) Making Home $743,000,000 Affordable (MHA) Primary Dealer $2,020,000,000,000 Credit Facility (PDCF) Term Securities $348,000,000,000 Lending Facility (TSLF) Term Auction $110,000,000,000 Facility (TAF) Temporary Liquidity $175,903,888,595 Guarantee Program (TLGP) Agency Mortgage- $184,950,000,000 Backed Securities Purchase Program (MBS) Asset-Backed $1,000,000,000 Commercial Paper Money Market Mutual Fund Liquidity Facility (AMLF) Commercial Paper $33,000,000,000 Funding Facility (CPFF) AIG Counterparty $2,300,000,000 TOTAL TARP $45,743,000,000 TOTAL Non-TARP $2,875,153,888,595 Non-TARP TARP – 29 –

Total Bailout Funding for Goldman Sachs: $874,552,426,455 Capital Purchase $10,000,000,000 Program (CPP) Primary Dealer $589,000,000,000 Credit Facility (PDCF) Term Securities $225,000,000,000 Lending Facility (TSLF) Temporary Liquidity $37,652,426,455 Guarantee Program (TLGP) AIG Counterparty $12,900,000,000 TOTAL TARP $10,000,000,000 TOTAL Non-TARP $864,552,426,455

Total Bailout Funding for JPMorgan Chase: $460,982,382,326 Capital Purchase $25,000,000,000 Program (CPP) Making Home $3,070,000,000 Affordable (MHA) Primary Dealer $112,000,000,000 Credit Facility (PDCF) Term Securities $68,000,000,000 Lending Facility (TSLF) Term Auction $99,000,000,000 Facility (TAF) Temporary Liquidity $42,512,382,326 Guarantee Program (TLGP) Asset-Backed $111,000,000,000 Commercial Paper Money Market Mutual Fund Liquidity Facility (AMLF) AIG Counterparty $400,000,000 TOTAL TARP $28,070,000,000 TOTAL Non-TARP $432,912,382,326 Non-TARP TARP – 31 – Total Bailout Funding

Total Bailout Funding for Morgan Stanley: $2,287,966,932,941 Capital Purchase $10,000,000,000 Program (CPP) Term Asset- $9,000,000,000 Backed Securities Loan Facility (TALF) Primary Dealer $1,913,000,000,000 Credit Facility (PDCF) Term Securities $115,000,000,000 Lending Facility (TSLF) Temporary Liquidity $30,256,932,941 Guarantee Program (TLGP) Agency Asset- $205,710,000,000 Backed Securities Purchase Program (MBS) Commercial Paper $4,000,000,000 Funding Facility (CPFF) AIG Counterparty $1,000,000,000 TOTAL TARP $19,000,000,000 TOTAL Non-TARP $2,268,966,932,941

Total Bailout Funding for Wells Fargo: $198,712,559,776 Capital Purchase $25,000,000,000 Program (CPP) Making Home $3,190,239,000 Affordable (MHA) Term Auction $159,000,000,000 Facility (TAF) Temporary Liquidity $10,022,320,776 Guarantee Program (TLGP) AIG Counterparty $1,500,000,000 TOTAL TARP $28,190,239,000 TOTAL Non-TARP $170,522,320,776

Citations

While people will undoubtedly argue forever about the amount or value of the many bailouts (separate and apart from the out of pocket costs), the truth is that there will never be agreement on a precise number. For example, what is the “value” of allowing Goldman Sachs and Morgan Stanley to become bank holding companies overnight in September 2008 when they were both admittedly just days away from bankruptcy? Similarly, what is the value of the Treasury guaranteeing the $3.7 trillion money market fund industry at the same time, i.e., putting the full faith and credit of the U.S. behind a single product for the first time in the history of the country? Or, what is the value of the U.S. guaranteeing $300 billion of Citigroup’s debt? More broadly, what is the value of the federal government providing assistance that literally made the difference between corporate survival or bankruptcy, as it did for AIG. And what is the value of the federal government de facto nationalizing all systemically important financial institutions, as it did with the issuance of an extraordinary joint press release in February of 2009. See Joint Press Release, Treasury, FDIC, OCC, OTS, and the Federal Reserve (Feb. 23, 2009), available at https://www. federalreserve.gov/newsevents/pressreleases/bcreg20090223a.htm.

Those are just a few examples of the innumerable and extraordinary financial rescues provided to the financial industry during the 2008 crash that simply cannot be quantified. In fact, they were undeniably priceless and unquantifiable, given that the alternative was a certain cascade of bankruptcies followed by financial and economic chaos and calamity. The best comprehensive approximation to date is that “the total Fed response was over $29 trillion.” See James Andrew Felkerson, A Detailed Look at the Fed’s Crisis Response by Funding Facility and Recipient, Public Policy Brief No. 123, at 4, LEVY ECONOMICS INSTITUTE OF BARD COLLEGE (2012) (“Levy Report”), https://www.econstor.eu/ bitstream/10419/121982/1/689983247.pdf. However, even if that study is off by a magnitude of 50%—which it is not—then it still means that around $15 trillion in bailouts were necessary.

Thus, the precise amount isn’t as relevant as its magnitude and long-term impact: It was inconceivably high and will be costing the U.S. and its people for a generation or more. 2 “Too-big-to-fail” is not just a metric for size but also shorthand for too complex, too interconnected, and too leveraged-to fail (as well as too-big-to-jail, too-big-to-manage, and arguably too-big-toregulate, subjects for another time). 3 Most people know this because the money they put in their savings account is guaranteed, up to a limit of $250,000, increased from $100,000 during the 2008 crash. It is noteworthy, however, that in 2007, the median savings balance in American was just $5,558, dropping to $3,912 in 2010. “Average U.S. Savings Account Balance 2019: A Demographic Breakdown,” available at https://www. valuepenguin.com/banking/average-savings-account-balance.

Those regulators included the FDIC, the Federal Reserve Board, the Office of the Comptroller of the Currency, the National Credit Union Administration, and, prior to 2010, the Office of Thrift Supervision. 5 See Better Markets, The Cost of the Crisis, $20 Trillion and Counting, at 70-87 (July, 2015) (“Better Markets Cost of the Crisis Report”), available at https://www.bettermarkets.com/sites/default/ files/Better%20Markets%20-%20Cost%20of%20the%20Crisis.pdf. 6 See Better Markets Cost of the Crisis Report. 7 None of the Six Megabanks reined in their runaway CEO pay either. Their CEOs have each continued to receive tens of millions of dollars in salary, bonuses, and other benefits every year since 2009, including the following amounts for 2018: • Bank of America – Brian Moynihan, Chairman and CEO – Salary, Bonus, and other Compensation: $26,500,000; • Citi – Michael Corbart, CEO – Salary, Bonus, and other Compensation: $24,183,714; Citations – 34 – • Morgan Stanley – James Gorman, Chairman and CEO – Salary, Bonus, and other Compensation: $29,000,000; • JP Morgan Chase – James Dimon, Chairman and CEO – Salary, Bonus, and other Compensation: $31,000,000; • Goldman Sachs – David Solomon, Chairman and CEO – Salary, Bonus, and other Compensation: $23,000,000; • Wells Fargo – Timothy J. Sloan, CED and President – Salary, Bonus, and other Compensation: $18, 426, 734. Contrast that to the unfortunate economic circumstances of tens of millions of American families who suffered and continue to suffer from the financial calamity that those very same banks caused.

The failure to effectively punish and deter illegal activity at the banks is the result of numerous weaknesses in the current approach to white collar crime on Wall Street. For example, monetary amounts, including penalties, although sometimes headline grabbing, typically represent just a fraction of a bank’s profits. Moreover, those amounts are typically significantly less than they appear because the settlements often assign unrealistically high values to future purported remedial actions (many of which the banks would have undertaken anyway) and because the settlements are usually structured to be largely tax deductible. And most importantly, rarely, if ever, are penalties brought to bear against the executives or individuals who preside over—and benefit enormously from—the bank’s illegal activities.

To the extent those executives insist they had no knowledge of the wrongdoing—and assuming that is even a credible claim—then it is clear that their banks are at least too-big-to-manage. Corporate leadership cannot have it both ways, protesting their innocence due to lack of knowledge while insisting that they are capable of managing such massive, sprawling, and unwieldy banks and that they deserve gigantic bonuses whenever the bank’s stock goes up. See Better Markets Blog, SEC Enforcement Has Incentivized, Rewarded & Guaranteed More Wall St Crime (Jan. 9, 2013) (highlighting the SEC’s failure to impose meaningful penalties or hold individual executives accountable), https://bettermarkets.com/blog/sec-enforcement-has-incentivized-rewardedguaranteed-more-wall-st-crime; see also, e.g., Better Markets Comment Letter re Proposed Guidance on Supervisory Expectation for Boards of Directors, (Feb. 15, 2018), https://bettermarkets.com/sites/ default/files/FRS-%20CL-%20BoD%20Supervison%20Expectations%202-15-18.pdf (highlighting the need for greater accountability and more rigorous supervisory expectations for boards of directors). 9 https://www.consumerfinance.gov/about-us/newsroom/cfpb-orders-bank-of-america-to-pay-727- million-in-consumer-relief-for-illegal-credit-card-practices. 10 http://investor.bankofamerica.com/phoenix.zhtml?c=71595&p=irol-newsArticle&ID=1960144&highli ght=#fbid=O91R7vDWm1g. 11 https://www.reuters.com/article/us-bankofamerica-settlement-idUSBREA361FJ20140407. 12 https://www.reuters.com/article/us-bankofamerica-overdraft-settlement/bofa-410-million-overdraftsettlement-wins-court-ok-idUSTRE74M63K20110523. 13 https://d9klfgibkcquc.cloudfront.net/Consent_Judgment_BoA-4-11-12.pdf. 14 https://www.reuters.com/article/bankofamerica-robocalls-settle/bank-of-america-in-record-settlementover-robocall-complaints-idusl1n0hq0hu20130930; https://www.law360.com/articles/572788/bofastrikes-historic-32m-settlement-to-end-tcpa-action. 15 https://www.justice.gov/opa/pr/bank-america-agrees-pay-1373-million-restitutionfederal-and-state-agencies-condition-justice; https://dealbook.nytimes.com/2010/12/07/ bofa-pays-137-million-to-settle-bid-rigging-charges/?mtrref=www.google. com&gwh=524BAC635CA95737ECF525BD8A2B32F3&gwt=pay. 16 https://www.reuters.com/article/us-bofa-lawsuit/bofa-pays-2-4-billion-to-settle-claims-over-merrillidUSBRE88R0PR20120928. 17 http://www.finra.org/newsroom/2013/finra-orders-wells-fargo-and-banc-america-reimburse-customersmore-3-million. 18 https://www.ftc.gov/news-events/press-releases/2002/09/citigroup-settles-ftc-charges-againstassociates-record-setting. 19 https://www.justice.gov/opa/pr/justice-department-federal-and-state-partners-secure-record-7-billionglobal-settlement. 20 https://www.justice.gov/opa/pr/five-major-banks-agree-parent-level-guilty-pleas. 21 https://www.consumerfinance.gov/about-us/newsroom/cfpb-orders-citibank-to-pay-700-million-inconsumer-relief-for-illegal-credit-card-practices/. 22 https://d9klfgibkcquc.cloudfront.net/Consent_Judgment_Citibank-4-11-12.pdf. 23 https://www.cftc.gov/PressRoom/PressReleases/7372-16. 24 https://www.sec.gov/litigation/admin/2015/33-9893.pdf. 25 https://dealbook.nytimes.com/2014/08/05/after-long-fight-judge-rakoff-reluctantly-approves-citigroupdeal/. 26 https://www.justice.gov/opa/press-release/file/967871/download. 27 https://www.sec.gov/news/press/2003-54.htm. 28 https://www.justice.gov/opa/pr/goldman-sachs-agrees-pay-more-5-billion-connection-its-sale-residentialmortgage-backed. 29 https://www.cftc.gov/sites/default/files/idc/groups/public/@lrenforcementactions/documents/ legalpleading/enfgoldmansachsorder122116.pdf. 30 https://www.sec.gov/news/press/2004-42.htm. 31 https://www.fhfa.gov/Media/PublicAffairs/PublicAffairsDocuments/2014%208%2022%20%20FHFAGoldman%20Sachs%20Settlement%20Agreement_Fannie%20Mae.pdf. 32 https://www.fhfa.gov/Media/PublicAffairs/PublicAffairsDocuments/2014%208%2022%20%20FHFAGoldman%20Sachs%20Settlement%20Agreement-Freddie%20Mac.pdf. 33 https://www.federalreserve.gov/newsevents/pressreleases/enforcement20180501b.htm. 34 https://ag.ny.gov/press-release/attorney-general-cuomo-announces-settlements-merrill-lynch-goldmansachs-and-deutsche. 35 https://www.sec.gov/news/press/2010/2010-123.htm. 36 https://www.sec.gov/litigation/admin/2016/34-76899.pdf. 37 https://www.fincen.gov/news/news-releases/jpmorgan-admits-violation-bank-secrecy-act-failed-madoffoversight-fined-461. 38 https://www.justice.gov/iso/opa/resources/69520131119191246941958.pdf. 39 https://www.nbcnews.com/businessmain/jpmorgan-pay-920-million-london-whale-probes4B11198211. 40 https://www.justice.gov/opa/pr/jpmorgan-chase-admits-anticompetitive-conduct-former-employeesmunicipal-bond-investments. – 35 – 41 http://www.nationalmortgagesettlement.com/files/Consent_Judgment_Chase-4-11-12.pdf. https:// www.justice.gov/opa/pr/federal-government-and-state-attorneys-general-reach-25-billion-agreement-fivelargest. 42 https://files.consumerfinance.gov/f/201309_cfpb_jpmc_consent-order.pdf. 43 https://www.sec.gov/news/press/2009/2009-232.htm. 44 https://www.sec.gov/news/press/2011/2011-131.htm; https://www.sec.gov/litigation/complaints/2011/ comp-pr2011-131-jpmorgan.pdf. 45 https://www.sec.gov/litigation/admin/2015/33-9992.pdf. 46 https://www.sec.gov/news/press/2003-159.htm. 47 https://www.justice.gov/opa/pr/morgan-stanley-agrees-pay-26-billion-penalty-connection-its-saleresidential-mortgage-backed. 48 https://www.cftc.gov/sites/default/files/idc/groups/public/@lrenforcementactions/documents/ legalpleading/enfmorganorder091514.pdf. 49 https://www.sec.gov/news/press/2005-10.htm. 50 https://www.fhfa.gov/Media/PublicAffairs/Documents/MorganStanleySettlementAgreement.pdf. 51 https://www.sec.gov/news/pressrelease/2017-46.html. 52 https://www.justice.gov/opa/pr/justice-department-requires-morgan-stanley-disgorge-48-million-53 profits-anticompetitive. 53 https://www.reuters.com/article/us-moodys-sp-settlement-wsj-idUSBRE93S11920130429. 54 https://www.sec.gov/litigation/admin/2017/33-10290.pdf. 55 https://www.reuters.com/article/us-wellsfargo-overdraft-decision-idUSBRE94E14320130515. 56 https://d9klfgibkcquc.cloudfront.net/Consent_Judgment_WellsFargo-4-11-12.pdf. 57 https://files.consumerfinance.gov/f/documents/cfpb_wells-fargo-bank-na_consent-order_2018-04.pdf. 58 https://money.cnn.com/2018/02/05/news/companies/wells-fargo-timeline/index.html. 59 https://www.justice.gov/usao-ndca/press-release/file/1084341/download. 60 https://files.consumerfinance.gov/f/201510_cfpb_stamped-exhibit-a-wells-consent-judgmentdocument-4-1.pdf. 61 http://www.finra.org/newsroom/2013/finra-orders-wells-fargo-and-banc-america-reimburse-customersmore-3-million ; http://www.finra.org/sites/default/files/fda_documents/2008014350501_FDA_ TX117236.pdf. 62 https://www.federalreserve.gov/newsevents/pressreleases/files/enf20110720a1.pdf. 63 https://money.cnn.com/2018/06/25/investing/wells-fargo-advisors-sec-settlement/index.html. 64 JPMorgan Chase has famously insisted that a bank’s balance sheet can be so strong that it becomes a “fortress” against instability.

The facts belie this claim for two reasons. First, as JPMorgan Chase itself learned from the so-called “London Whale” fiasco, huge and sudden losses can take any bank by surprise, resulting in multi-billion-dollar losses. See Tom Braithwaite, Tracy Alloway, and Shahien Nasiripour, JP Morgan to boost “fortress” balance sheet, WALL ST. J. (Mar. 8, 2013). Such an isolated event at a single bank during market tranquility is not likely to be systemic; however, such things happen at unpredictable times and can, as Morgan Stanley experienced in December 2007, coincide with burgeoning subprime losses that accelerate catastrophic capital losses. Second, the history of the 2008 crash itself vividly demonstrated that even institutions thought to be impervious to crisis – 36 – suddenly faced collapse due to the contagious effects of the crash and the interconnected nature of the financial system, among other things. 65 See Better Markets Cost of the Crisis Report, at 66-69. 66 https://www.investopedia.com/terms/c/capital-purchase-program.asp. 67 https://www.treasury.gov/initiatives/financial-stability/TARP-Programs/bank-investment-programs/tip/ Pages/default.aspx. 68 https://projects.propublica.org/bailout/programs/6-making-home-affordable; https://www.treasury.gov/ initiatives/financial-stability/TARP-Programs/housing/mha/Pages/default.aspx. 69 https://www.treasury.gov/initiatives/financial-stability/TARP-Programs/credit-market-programs/talf/ Pages/default.aspx;https://projects.propublica.org/bailout/programs/7-term-asset-backed-securities-loanfacility. 70 https://www.investopedia.com/terms/t/term-auction-facility.asp. 71 https://www.federalreserve.gov/monetarypolicy/tslf.htm. 72 https://www.federalreserve.gov/regreform/reform-pdcf.htm. 73 https://www.federalreserve.gov/regreform/reform-amlf.htm. 74 https://www.federalreserve.gov/monetarypolicy/cpff.htm. 75 https://www.fdic.gov/regulations/resources/tlgp/index.html. 76 https://projects.propublica.org/bailout/list. 77 https://www.gao.gov/new.items/d11696.pdf. 78 FDIC, Crisis and Response, An FDIC History, 2008-2013 (Nov. 2017), https://www.fdic.gov/bank/ historical/crisis/. We drew on the FDIC report for data reflecting the Six Megabanks’ reliance on the Temporary Liquidity Guarantee Program. 79 See Levy Report. In particular, the Levy Report showed that Morgan Stanley and Citigroup received $205.71 billion and $184.95 billion respectively through their participation in the Agency MortgageBacked Securities Purchase Program. See Levy Report at 17-18. The Levy report indicates that Goldman and JPMorgan Chase also benefited from participation in the program, although it does not provide exact amounts. 80 It was in connection with this restructuring that Citi became the only megabank not to repay $25 billion of its total $45 billion TARP cash infusion; Treasury was “repaid” $25 billion via a stock issuance. See Henry Blodget, Citigroup Does The Impossible:

It Screws US Taxpayers Again, BUSINESS INSIDER (Dec. 7, 2009), https://www.businessinsider.com/henry-blodget-citigroup-does-the-impossibleit-screws-us-taxpayers-again-2009-12; CBS News, Citigroup to Repay $20B in Bailout Money, (Dec. 14, 2009), https://www.cbsnews.com/news/citigroup-to-repay-20b-in-bailout-money/. 81 See Better Markets, Goldman Sachs Failed 10 Years Ago Today; Email Shows Goldman Admitted It Was “Toast” and Only Survived Due to Government Bailouts (Sept. 20, 2018), available at https:// medium.com/@BetterMarkets/goldman-sachs-failed-10-years-ago-today-2097a82b6f2. The email was from Michael Silva who was the chief of staff and senior vice president for the Executive Group at the New York Fed, and it relates to a phone call from Morgan Stanley (MS) to Timothy F. Geithner (TFG), then President of the Federal Reserve Bank of New York, about it and Goldman Sachs (GS). Source

The law taught an important spiritual lesson. For a lender to forego interest on a loan to a poor person would be an act of mercy. He would be losing the use of that money while it was loaned out. Yet that would be a tangible way of expressing gratitude to God for His mercy in not charging His people “interest” for the grace He has extended to them. Just as God had mercifully brought the Israelites out of Egypt when they were nothing but penniless slaves and had given them a land of their own (Leviticus 25:38), so He expected them to express similar kindness to their own poor citizens.

Christians are in a parallel situation. The life, death, and resurrection of Jesus has paid our sin debt to God. Now, as we have opportunity, we can help others in need, particularly fellow believers, with loans that do not escalate their troubles. Jesus even gave a parable along these lines about two creditors and their attitude toward forgiveness (Matthew 18:23-35).

The Bible neither expressly forbids nor condones the borrowing of money. The wisdom of the Bible teaches us that it is usually not a good idea to go into debt. Debt essentially makes us a slave to the one who provides the loan. At the same time, in some situations going into debt is a “necessary evil.” As long as money is being handled wisely and the debt payments are manageable, a Christian can take on the burden of financial debt if it is absolutely necessary. Source

: We have all seen the headlines: multiple bank and business bailouts, rising home foreclosures, jobs lost and firms downsizing, 401ks and IRAs dropping in value, rising utility, grocery, and gasoline prices. What are Christians supposed to do when we’re hit by a national or personal financial crisis?

How we weather a financial storm depends mostly on our attitude about whom the money belongs to in the first place. Do we view our money as ours? Or do we view it as coming from and belonging to God? If we see our income as being from the Lord, it makes it much easier to navigate the turbulent waters of economic downturns and tough financial situations. Whether we lose or make money, it is all His and under His control, and that is a truly freeing concept.

The Lord created all of us with certain talents and gifts which we are to use to not only make a living, but to also help us live our lives in such a way as to bring glory and honor to Him (Romans 12:1-2; 1 Corinthians 6:20). So while we grow up, follow our individual career paths into adulthood, and begin our lives as contributing members of society, making money and accumulating possessions along the way, we are also to serve and worship the Lord with every fiber of our being. We cannot do that if we consider it all ours and not His.

We will always find ourselves serving what we treasure the most, whether it is wealth, power, fame, or the Lord. The Bible shows us that Jesus well knew the lure of money and possessions because during His earthly ministry He actually spoke more on the subject of finances than on heaven and hell combined. Luke 12:15-34is an excellent passage on the attitude we should have toward our money and possessions and is well worth taking some time to prayerfully read and study.Source

StevieRay Hansen

Editor, Bankster Crime

MY MISSION IS NOT TO CONVINCE YOU, ONLY TO INFORM…